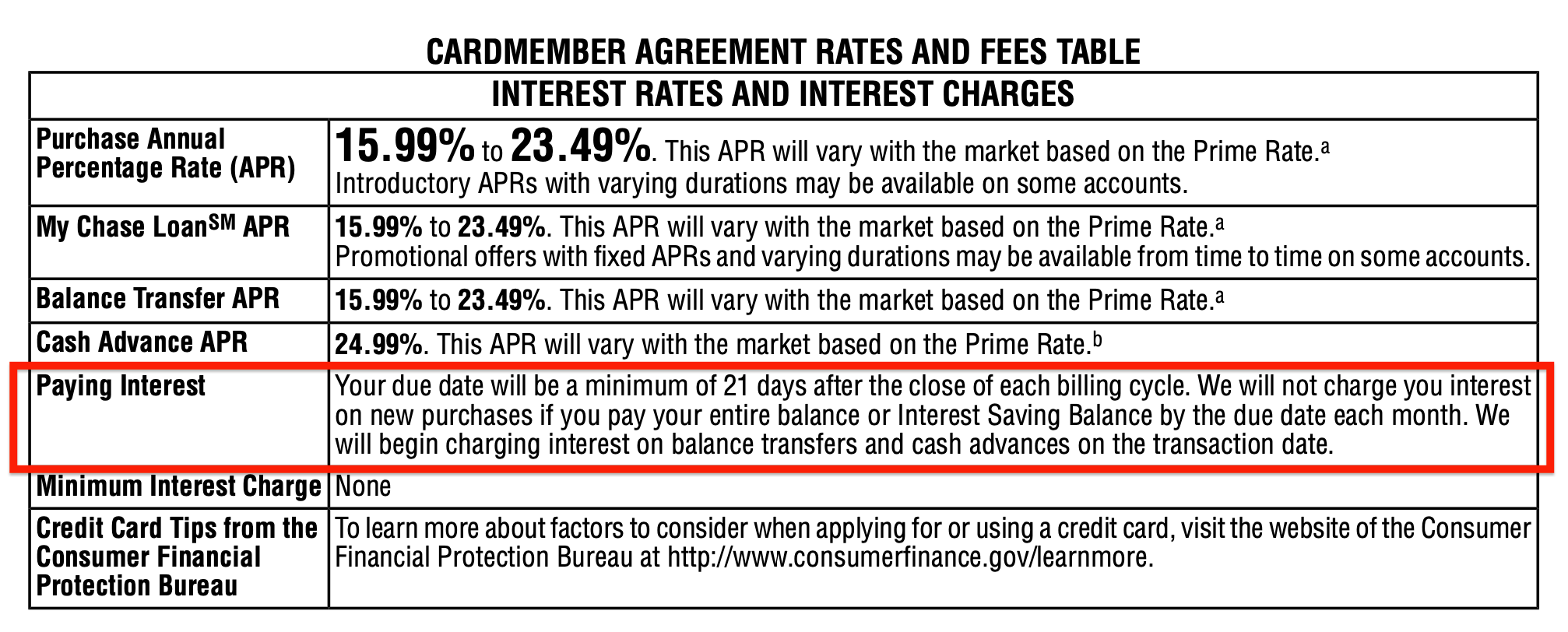

Representative website links into the affairs in this post are from partners one compensate united states (get a hold of all of our advertiser disclosure with the help of our a number of lovers for much more details). But not, the viewpoints is actually our own. Observe we rate mortgages to type objective ratings.

- From inside the 2024, you might acquire as much as $766,550 having a compliant loan.

- So you’re able to acquire over the new FHFA allows for compliant money, envision making an application for an excellent jumbo mortgage.

- The newest standard conforming loan limit when you look at the Alaska, Their state, Guam, as well as the United states Virgin Isles are $1,149,825.

From year to year, the fresh Government Casing Money Institution (FHFA) changes extent you might obtain having a conforming financing, which you probably remember once the good “normal mortgage.”

Standard conforming financing limitations

During the 2024, you could potentially obtain to $766,550 into a compliant mortgage in the most common portion, establishing a compliant financing limit increase out of $forty,350 out-of last year’s numbers. They are borrowing from the bank restrictions for single-unit land, but you can obtain a whole lot more for a few-device ($981,500), three-device ($step one,186,350), and you will five-product residential property ($step 1,474,400).

If you need to acquire a lot more

If you would like acquire over new FHFA allows, good jumbo mortgage is an option. Jumbo fund are simply mortgages for individuals who you desire over the fresh new FHFA normally lets. They typically has more strict qualifications standards to help you qualify for a mortgage and better interest rates than just compliant funds. Jumbo financing was riskier to have lenders, very people enable it to be harder so you can be considered to reduce the alternative of a debtor defaulting towards the payments.

For every single lending company features its own criteria to have jumbo fund, but you’ll most likely you prefer a good credit score, a diminished loans-to-earnings proportion, and you will a more impressive down payment than simply you might for a compliant loan. Expect you’ll you desire at the least a beneficial 700 credit score and you will 20% or even more to have a down payment. In addition may need a debt-to-income (DTI) ratio regarding 36% in order to forty five%.

The greater your credit score, DTI proportion, and you may deposit, the greater amount of you will be accepted to help you obtain with a good jumbo loan.

For people who be eligible for a conforming loan

![]()

Whenever you be eligible for a compliant mortgage – and acquire a home you adore in compliant financing limitations – it can have many positives. Interest rates usually are straight down into conforming financing than the non-conforming and you will jumbo money, while will often have a broader group of lenders, too, as these financing are particularly prominent.

If not be eligible for a conforming or jumbo mortgage, it’s also possible to get a keen FHA financial, that is for those who have credit scores as low as 580 and you will a great DTI proportion out of 43% otherwise down. The newest borrowing limit relies on where you happen to live, and find the restrict for your county right here.

You’ll be able to be eligible for an excellent Virtual assistant home loan if you are a military affiliate, or good USDA home loan if you are to purchase when you look at the an outlying city. None ones kind of home loans means a down payment. Va mortgages don’t possess a credit limit, and USDA mortgage loans normally have an identical limits given that compliant financing.

Faq’s regarding the compliant financing constraints

Yes, the new conforming financing restrictions transform a year. The latest Federal Construction Funds Department changes them predicated on housing market requirements and you will local money style. Visit to see the 2024 conforming financing constraints by state.

Zero, FHA mortgage limitations are not the same given that compliant loan limits. This new limitations into the FHA funds are usually below conforming financing limitations. Such as for instance, FHA loan constraints inside 2024 is actually $498,257 on its low; compliant loan standard constraints exceed $700,000.

If or not you should buy a conforming financing having the lowest credit rating utilizes a few things. Conforming financing tend to have stricter criteria than other mortgage applications, so that you typically you would like a very good credit history – on 680 – to help you meet the requirements. You might be able to find a conforming financing that have a great lower rating, you can expect to pay increased interest rate in the event the you are doing.

A good jumbo loan is a kind of home loan that lets you borrow over the conforming mortgage maximum. These are usually Arizona installment loans online much harder in order to qualify for and want more substantial down-payment.

Conforming finance meet with the being qualified standards set-out from the Fannie mae and you can Freddie Mac computer and you may end up in the fresh conforming loan limitations to own the area. Non-conforming money might have larger financing limitations but they are typically more complicated so you’re able to be eligible for.